Global trade is undergoing a profound transformation. While liberalization once unified markets, a resurgence of strategic nationalism is now fragmenting regulatory regimes. Protectionism, digital rules, and export controls are reshaping the global economic order, raising costs, complicating compliance, and challenging the multilateral framework that

once defined it

By NEERAJ KANSAL, Pr. Addl. Director General, Central Board of Indirect Taxes & Customs

Snapshots

- Developing nations view EU’s CBAM as “green protectionism,” unfairly penalizing exporters who lack the required sustainable infrastructure

- Strategic reforms and diversified exports are vital for India to mitigate trade impacts and achieve its $7 trillion economic goal

- India’s industrial policy combines targeted protection with export incentives, balancing autonomy with global economic integration

- Regulations must protect without causing paralysis; nations should prioritize sovereignty without retreating into economic isolation

THE ever-growing global economy is facing a paradox: while market liberalisation and globalisation have historically driven growth, there is now a visible return to reassessing regulatory frameworks, often prompted by domestic political compulsions, economic insecurities, and geopolitical dynamics.

For decades, the state has retreated from economic management, granting markets greater freedom. However, recent years have witnessed a resurgence of the regulatory state, particularly in sectors deemed strategic, such as energy, digital infrastructure, defence, and food security, and occasionally in non-strategic sectors, often due to catering to certain vested interests or promoting supporters. Nations cite their actions as being influenced by national security concerns or environmental sustainability mandates. Additional factors include supply chain vulnerabilities and the rise of social media and digital misinformation.

We have endeavoured to unpack the complexity of the rising regulatory conundrum: why states are re-regulating, what contradictions it creates, and how it affects both domestic and international economic systems.

FROM HARMONISATION TO FRAGMENTATION

Global trade has long relied on a degree of harmonisation, facilitated by institutions such as the World Trade Organization (WTO) and agreements like the General Agreement on Tariffs and Trade (GATT). However, the past decade has witnessed a shift towards regulatory fragmentation, driven by various factors. These factors have created a regulatory mosaic, forcing businesses to navigate a labyrinth of rules that vary by country, sector, and even product type. The cost of compliance is staggering: a 2023 WTO report estimated that trade barriers and regulatory misalignment increase the cost of cross-border transactions by 10–20%.

There is a surge of Economic Nationalism, with countries increasingly prioritising domestic industries through protectionist measures. For instance, the United States’ tariffs on Chinese goods during the U.S.-China trade war (2018–2020) and India’s “Make in India” initiative reflect a trend towards self-reliance, often at the expense of global supply chains.

GREEN POLICIES RESHAPING TRADE

Geopolitical rivalries and brewing tensions, such as the U.S.-China decoupling or sanctions on Russia following the 2022 invasion of Ukraine, have led to trade restrictions and export controls. These measures, while politically motivated, fragment global markets by creating compliance hurdles for multinational corporations.

In response to the push for sustainability, many countries have armed themselves with potential

Environmental and Social Regulations, prompting the adoption of stringent environmental standards, such as the European Union’s Carbon Border Adjustment Mechanism (CBAM), set to be fully implemented in 2026. While aimed at reducing carbon emissions, by imposing tariffs on carbon-intensive imports to prevent “carbon leakage”, such regulations create disparities, as not all countries possess the requisite infrastructure to comply. While environmentally progressive, it places a burden on exporters from developing nations like India and South Africa, which rely on carbon-heavy industries. These countries argue CBAM is a form of “green protectionism”, highlighting tensions between environmental goals and trade equity.

Global trade has long relied on a degree of harmonisation, facilitated by institutions such as the World Trade Organization (WTO) and agreements like the General Agreement on Tariffs and Trade (GATT). However, the past decade has witnessed a shift towards regulatory

fragmentation, driven by various factors

The COVID-19 pandemic exposed vulnerabilities in global supply chains, prompting countries to impose stricter health, safety, and supply chain resilience regulations. For example, export bans on medical supplies during 2020–2021 disrupted global markets. This increasing re-regulation presents several contradictions:

Protectionism vs. Competitiveness: While aiming to protect local industries, overregulation can undermine their ability to compete globally by stifling the development of innovative and globally competitive product ranges and services.

Sovereignty vs. Multilateralism: Regulatory choices often conflict with WTO and bilateral trade

agreements.

Short-term Populism vs. Long-term Growth: Regulatory populism can yield electoral dividends but may harm innovation and investment, affecting the overall growth of the country leading to challenging trade-offs and decisions.

EXPORT CONTROLS RESHAPING TRADE

Export controls are evolving rapidly, driven by technological advances and shifting geopolitical dynamics. Three major trends are shaping the current and future landscape of export restrictions:

The Proliferation of Controls: The sheer number and scope of export controls are expanding.

Governments are continuously adding new products and technologies to their control lists. For example, encryption technologies once considered outdated, remain controlled due to their potential military applications. More recently, one can see U.S.-China Tech war whereby emerging fields such as artificial intelligence and semiconductor manufacturing equipment have become central targets of export restrictions aimed to curb China’s technological rise.

These controls, expanded in 2022 and 2023, have forced global tech firms to comply with complex licensing requirements, disrupting supply chains and raising costs. China’s retaliatory restrictions on critical minerals like gallium further complicate the puzzle. This expansion complicates compliance, as companies must track an ever-growing list of controlled items and navigate varying regulations across jurisdictions.

The Fracturing of Traditional Alliances: The global consensus that once underpinned multilateral export control regimes is fracturing. Historically, countries coordinated controls through organizations like the Wassenaar Arrangement to maintain a level playing field. However, rising geopolitical tensions and technological competition have led to divergent approaches. The United States, for instance, has formed coalitions to impose targeted controls in response to conflicts such as Russia’s invasion of Ukraine, while also excluding some allies from certain restrictions. This fragmentation creates a patchwork of rules that complicates strategic planning and compliance for multinational companies requiring them to implement robust monitoring and compliance systems.

The Growing Use of Extraterritorial Authority: The extraterritorial application of export controls is becoming more common. Countries are extending their regulatory reach beyond their borders to govern foreign-made products containing controlled domestic content or technology. The United States enforces this through rules like the “de minimis” and “foreign-produced direct product” provisions, which capture items with a certain percentage of U.S.-origin components or technology. China has adopted similar measures, and the European Union now requires companies to ensure their products do not reach sanctioned destinations such as Russia and Belarus.

Together, these trends are transforming export controls from static, narrowly focused rules into

dynamic, multifaceted regulatory regimes that demand agility, foresight, and strategic adaptation from businesses operating internationally.

DOUBLE-EDGED SWORD OF MODERN TRADE REGULATIONS

Any regulation in any form has far-reaching consequences for global trade dynamics, including increased costs and complexity, supply chain disruptions, and a sacrifice of the concept of multilateralism in favour of regionalism or favoured nations. Furthermore, developing nations, with limited capacity to meet stringent standards like the EU’s CBAM or U.S. sanctions compliance, face reduced market access, exacerbating global economic inequalities. Many countries have also adopted “supply‐chain nationalism” – guaranteeing priority for domestic firms in government contracts or essential goods (vaccines, medical supplies, food).

Companies face higher operational costs due to compliance with diverse standards. Small and

medium-sized enterprises (SMEs), lacking the resources of multinational corporations, are particularly disadvantaged, which reduces their ability to compete globally.

The sheer number and scope of export controls are expanding. Governments are continuously adding new products and technologies to their control lists. For example,

encryption technologies once considered outdated, remain controlled due to their potential military applications

Multilateral trade rules (WTO) are under strain, with disputes stalled and new plurilateral agreements covering only subsets of members. The proliferation of unilateral regulations undermines multilateral trade agreements. The WTO’s dispute settlement mechanism, already weakened by the U.S. blocking appellate body appointments, struggles to address conflicts arising from divergent regulations. As navigating global regulations becomes untenable, companies are shifting towards regional supply chains. The Regional Comprehensive Economic Partnership (RCEP) in Asia and the African Continental Free Trade Area (AfCFTA) exemplify this trend, but they also risk creating trade blocs that further fragment the global economy.

The U.S. CHIPS Act seeks to onshore semiconductor production but violates free-market principles. China’s data sovereignty laws insulate its tech ecosystem but discourage foreign partnerships. Regulatory divergence forces companies to reconfigure supply chains. For example, U.S. restrictions on semiconductor exports to China have pushed firms to diversify sourcing, often at higher costs, contributing to global chip shortages.

While that be so, regulations can promote fair trade, protect consumers, and ensure environmental sustainability, like the European Union’s General Data Protection Regulation (GDPR) which lays new standards for data protection, while the U.S. Environmental Protection Agency(US EPA) regulates emissions and pollution.

Each instance reflects the trade-off between strategic autonomy and global economic cohesion. This has reduced the world to a Global Trade puzzle, with sectoral and mutual treaties gaining momentum in place of an Open for all policy.

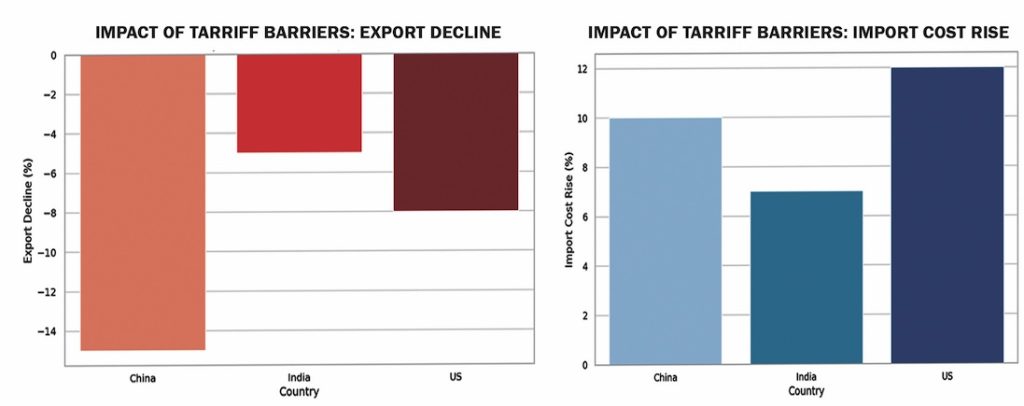

WEIGHING GDP IMPACTS

Regulating trade through tariffs, sanctions, or restrictions under pretexts like terrorism, balance of trade, or retaliation has significant implications for global GDP. Above is an analysis of these effects in the Indian context, building on the global perspective and incorporating relevant data.

These visuals support the argument on how protectionist policies, even if politically motivated, introduce real economic costs.

As noted globally, trade barriers like tariffs and sanctions reduce global GDP by increasing costs and disrupting supply chains. The IMF estimated that the U.S.-China trade war cost global GDP $1.7 trillion by India, as a major emerging economy, is affected by these disruptions, particularly in its export markets like the U.S. and EU, which account for a significant share of its trade (e.g., 40.17% of exports in 2006-07 went to top destinations like the U.S., UAE, and China). India’s trade (goods and services) as a percentage of GDP has risen from 15.7% in 1990 to 48.1% in 2022-23, reflecting growing integration into the global economy.

However, protectionist measures globally or domestically can dampen this, reducing India’s GDP growth. For instance, a 10% global tariff increase could shave 1-2% off global GDP annually, with India potentially losing 0.5-1% of GDP due to its reliance on exports (22.4% of GDP in 2022-23).

INDIA’S TRADE JOURNEY

Before economic liberalisation in 1991, India’s high tariffs (over 200%) and import restrictions stifled trade, keeping exports at 6.9% of GDP in 1990-91. This led to inefficiencies and slow growth, with GDP per capita at $3,800 (PPP) in 2006.

Since the 1991 reforms, tariff reductions (from 125% in 1990-91 to 13.4% in 2016) and liberalisation have boosted India’s GDP growth, reaching 8.2% in FY23-24 and making India the fifth-largest economy ($3.57 trillion in 2023). Liberalisation since 1991 has attracted $82 billion in FDI in 2021-22, enhancing sectors like finance and R&D. Free trade agreements (e.g., with UAE and Australia) have driven double-digit export growth, with a 25% rise in gems and jewellery exports to UAE post-CEPA.

SHIFTING GLOBAL TIDES: OPPORTUNITY AND RISK

For India, these immediate global currents are double-edged. On the plus side, rising U.S. import tariffs and China’s tech export curbs have shifted some business to Indian exporters. Indeed, India is benefiting from a “China+1” strategy; consequently, exports of pharmaceuticals, software services, and certain engineering goods have surged, as new markets in Africa, Latin America, and East Asia are opening for Indian products. On the downside, fragmented rules abroad mean Indian exporters face a bewildering array of standards.

India is leveraging its Digital Public Infrastructure (DPI) to set new global standards. With 16.7 billion transactions in 2024, India is exporting its fintech model as a “bridge” between different regulatory regimes

India has faced and responded to trade barriers. For example, in response to U.S. tariffs on Indian steel and aluminium, India proposed retaliatory duties on $7.5 billion of U.S. imports under WTO norms in 2025, potentially escalating costs for Indian consumers and industries reliant on U.S. goods. Deloitte estimates that a proposed 16% reciprocal U.S. tariff could reduce India’s GDP growth by 0.1-0.3% in FY25-26, offsetting gains from domestic tax incentives (0.6-0.7% GDP boost).

TRADE DEFICIT CHALLENGES

India has run a persistent trade deficit since the 1980s, driven by high imports of oil, electronics, and commodities. In 2022-23, imports reached $892 billion against exports of $776 billion, with the trade deficit at 3.3% of GDP. Protectionist policies, like high tariffs to “balance trade,” often backfire by raising input costs for Indian manufacturers, decreasing competitiveness. For instance, India’s import-heavy industrialisation and reliance on Chinese electronics widen this gap, exacerbated by global supply chain disruptions (e.g., post-COVID and the Russia-Ukraine conflict). However, recent protectionist moves, like India’s restrictions on $770 million of Bangladeshi imports in 2025, risk tit-for-tat responses, potentially harming regional trade and GDP.

India’s manufacturing sector, at 15% of GDP, lags behind due to low R&D investment and

technological gaps, worsened by trade barriers limiting access to advanced inputs. Policies like the National Manufacturing Policy (2011) aim for 12-14% growth, but global trade restrictions hinder progress.

India’s trade-to-GDP ratio (48.1% in 2022-23) and its ranking as the 8th-largest exporter globally demonstrate its growing role in the world economy. However, protectionist policies, whether globally or domestically, could reverse these gains.

Digital Trade and Data Governance

Digital trade, primarily through data services and e-commerce across borders, is demonstrating

impressive growth. Advances in AI, fintech, and data analytics have made data the lifeblood of modern trade. The digital economy and consequent data governance issues have introduced new regulatory challenges. International e-commerce exports are anticipated to reach a value of $2 trillion by 2025, accounting for 10% of global trade volume. Chinese cross-border e-commerce platforms, such as Shein and Temu, have emerged rapidly, currently capturing 40% of the global market share, and are expected to expand further by 2025, posing a formidable challenge to traditional retail.

CHALLENGES FROM REGULATIONS

Despite this growth, the divergences in technical standards and data privacy protection among the U.S., the European Union, and China are becoming increasingly noticeable, as exemplified by the EU’s General Data Protection Regulation (GDPR) and China’s Data Security Law and Personal Information Protection Law (PIPL) which impose strict data localisation and privacy requirements, complicating cross-border data flows. These differences constitute new “digital barriers” that limit the further development of digital trade.

Globally, a key flashpoint has been the WTO e-commerce moratorium – a long-standing pause on levying customs duties on cross-border digital transmissions. In 2023, the moratorium lapsed as India (joined by South Africa) insisted on preserving the right to levy duties on digital imports, arguing that the status quo unfairly limits the tariff revenue of developing countries. Critics say this stance could invite retaliation and higher digital trade costs. In reality, India’s current digital sector is not a significant tariff earner yet (the IMF notes that removing the moratorium could yield up to ~$10B annually for developing countries, primarily through taxing developed-country digital services). India’s position reflects a development perspective: it seeks the fiscal space to tax big tech if necessary, unless wealthier nations offer better compensation or development assistance.

DATA PROTECTIONISM AND GLOBAL E-COMMERCE

Domestically, India is also overhauling its data rules. The new Digital Personal Data Protection Act, 2023 seeks to balance privacy with innovation. It exempts inbound data flow from onerous restrictions (to maintain the flow of imported digital services), while requiring Indian firms to store and protect data. This law was passed after consultations with the EU, which now views India as a data governance partner (they issued a joint declaration on data flows in 2021).

India is also actively shaping global rules – another use of soft power. It has been a participant in the Joint Statement Initiative on E-commerce (though it did not sign the latest 2024 agreement, it engaged in the negotiations).

It champions proposals at the WTO regarding digital public infrastructure (India’s own UPI system serves as a model) and aids least-developed countries in connection efforts. Notably, India promotes interoperability of data rules – using techniques like “model clauses” or regulatory sandboxes – to bridge different regimes. For instance, India’s involvement in the G20 working groups has emphasised “data free flow with trust.” By presenting itself as a technology-harnessing emerging economy, India is countering the notion that data flows should be confined behind walls. This stance is gradually earning allies among other developing nations seeking data-driven growth. The result of these endeavours is that India’s digital economy is thriving even amid fragmentation. Over 1.3 billion Indians possess Aadhaar digital IDs, and

more than 900 million people utilise the UPI payment system (16.7 billion transactions in 2024). E-commerce in India – despite facing some new foreign investment regulations – still grew by double digits recently, driven by fintech and homegrown startups. These facts highlight that India’s digital strategy is not to isolate itself but to establish a strong base and good governance so that it can compete and collaborate in a fragmented digital world.

Carving India’s Trade Future

Strategic reforms, diversified exports, and robust trade agreements are critical for India to mitigate these impacts and sustain its trajectory toward a $7 trillion economy by 2030.

To minimise negative GDP impacts, India could:

➢ Enhance Trade Agreements: Pursue ambitious trade deals (e.g., with the EU, UK, and Oman) to boost exports.

➢ Diversify Exports: Move beyond traditional commodities (e.g., petroleum, engineering goods) to high-value sectors like electronics and renewables.

➢ Improve Logistics: Policies like the National Logistics Policy reduce trade costs, supporting GDP growth.

➢ Balance Protectionism: While some protection is needed, excessive tariffs or bans may invite

retaliatory measures and higher costs, as seen in India’s response to U.S. tariffs. As can be seen, India offers a compelling illustration of this conundrum: While promoting “Ease of Doing Business,” it has simultaneously increased compliance obligations. FDI-friendly rhetoric contrasts with frequent policy shifts and opaque regulatory environments. Industrial policies under Atmanirbhar Bharat aim for self-reliance but have raised concerns among global investors and trading partners. India is not retreating into isolation; rather, it is “calibrating” its openness.

By targeting protection to strategic areas (semi-conductors, chemicals, defence) while simultaneously bolstering export competitiveness, the goal is to achieve self-reliance without sacrificing global integration.

In this, India’s fiscal tools (like PLI subsidies, credit support) are being aligned with trade policy, ensuring that protection comes with a clear plan for productivity gains and eventual export

readiness. This balanced stance, protect selectively, but globalise quickly—is the hallmark of India’s evolving strategy in the face of rising protectionism.

The U.S. CHIPS Act seeks to onshore semiconductor production but violates free-market principles. China’s data sovereignty laws insulate its tech ecosystem but discourage foreign partnerships. Regulatory divergence forces companies to reconfigure supply chains

THE PATH AHEAD: “SMART REGULATION”

Scholars and policymakers argue that the answer lies in “smart regulation”:

- Rules that foster innovation, not stifle it.

- Selective protectionism with global collaboration.

- Strong, transparent, and accountable regulatory institutions.

Resolving the regulatory conundrum requires balancing national priorities with global cooperation. International bodies like the WTO or OECD could facilitate dialogues to align standards, particularly in emerging areas like digital trade and sustainability. Institutions like WTO and WCO need urgent reform to stay relevant with better dispute resolution mechanisms, inclusion of digital economy norms and stronger enforcement.

Mutual recognition agreements, where countries accept each other’s standards as equivalent, could reduce compliance burdens.

For the larger good of the world, Capacity Building for Developing Nations is essential. Wealthier

nations and international organizations should invest in helping developing countries meet stringent regulations. For instance, technical assistance for CBAM compliance could ensure equitable trade access.

The answer also lies in Regulatory Whiplash which means policy consistency. Constant flip-flops or surprise curbs unsettle markets and businesses and thus regulatory reform should be consultative and phased, not sudden or reactionary.

The point to bring home is that Strategic autonomy and global cooperation can coexist. A calibrated approach, protecting critical sectors while being open in others, is ideal.

“Self‐reliance is wise, but isolation is costly.”

The global trade puzzle, driven by a surge in regulatory divergence, presents significant challenges to economic efficiency, equity, and cooperation. While national priorities like economic security, environmental sustainability, and technological sovereignty are valid, the resulting fragmentation risks undermining the advantages of globalisation. Addressing this conundrum necessitates a delicate balance: fostering cooperation without stifling sovereignty, and promoting fairness without sacrificing innovation. By pursuing regulatory convergence, capacity building, and multilateral reform, the world can start to assemble a more cohesive trade framework, one that navigates the complexities of the 21st century while preserving the interconnectedness that propels global prosperity.

Regulation is essential, but excessive or poorly designed regulation can become a self-imposed barrier. Nations must walk a tightrope, ensuring balance in sovereignty and security without retreating into economic isolation. The real challenge is to design governance systems that are nimble, inclusive, and forward-looking, not regressive.